All Categories

Featured

Table of Contents

You can make a partial withdrawal if you require added funds. Furthermore, your account value continues to be kept and credited with present interest or financial investment earnings. Naturally, by taking regular or methodical withdrawals you risk of diminishing your account value and outlasting the contract's built up funds.

In many agreements, the minimum interest rate is evaluated issue, yet some contracts permit the minimal price to be adjusted regularly. Excess passion agreements offer versatility with respect to costs settlements (single or versatile). For excess rate of interest annuities, the maximum withdrawal cost (also called a surrender charge) is capped at 10%.

A market price modification changes an agreement's account worth on surrender or withdrawal to reflect adjustments in interest rates because the receipt of agreement funds and the remaining duration of the rate of interest price guarantee. The adjustment can be positive or adverse. For MGAs, the maximum withdrawal/surrender fees are shown in the following table: Year 1Year 2Year 3Year 4Year 5Year 6Year 7Year 8 and Later7%6%5%4%3%2%1%0%Like a deposit slip, at the expiration of the warranty, the accumulation amount can be renewed at the business's brand-new MGA rate.

Ira Fixed Annuities

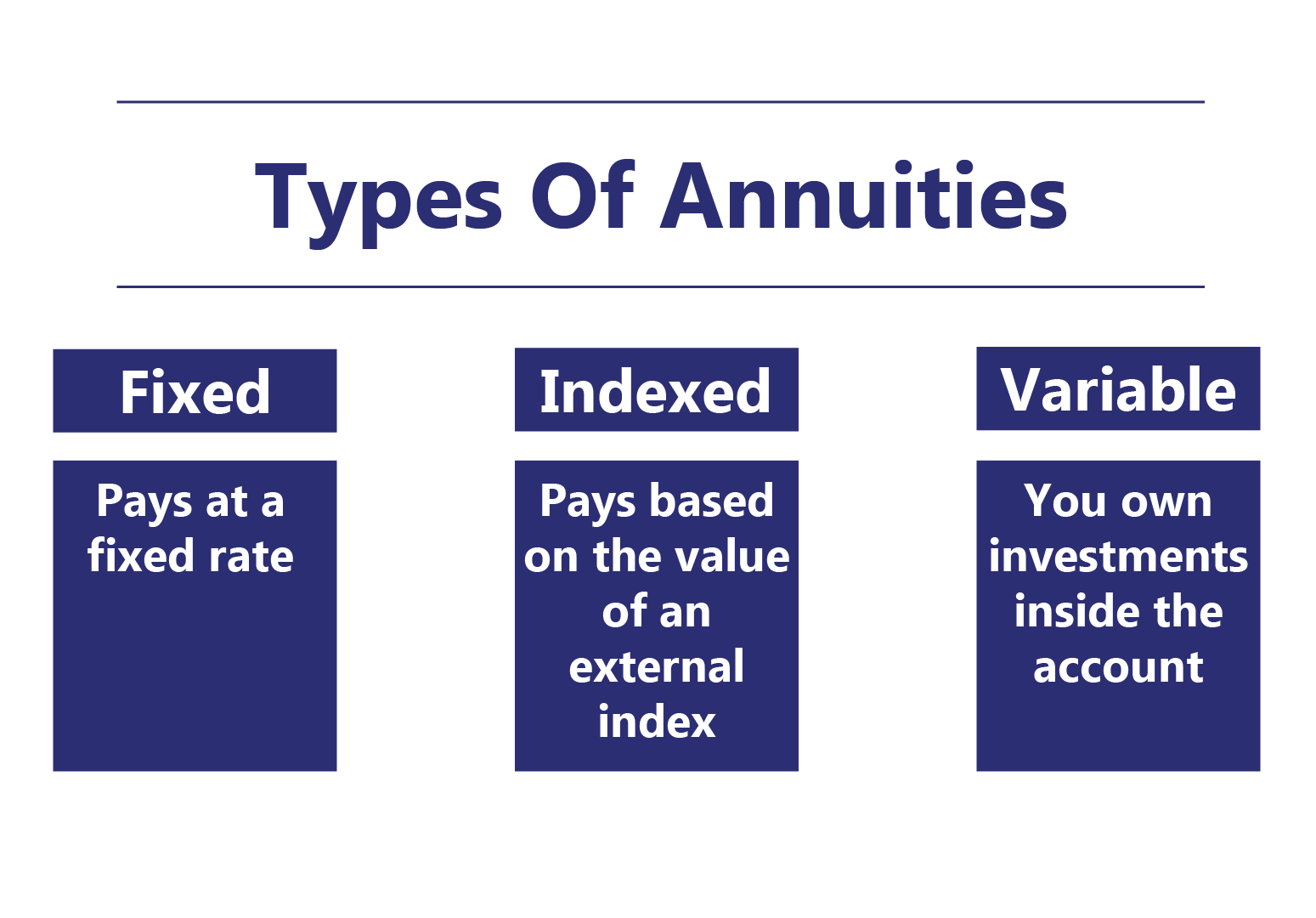

Unlike excess passion annuities, the quantity of excess interest to be credited is not known up until the end of the year and there are typically no partial credit reports during the year. Nonetheless, the technique for establishing the excess passion under an EIA is identified ahead of time. For an EIA, it is essential that you understand the indexing features utilized to determine such excess rate of interest.

You need to additionally understand that the minimal floor for an EIA varies from the minimum flooring for an excess interest annuity - annuity and life (annuity versus life insurance). In an EIA, the flooring is based upon an account worth that might attribute a lower minimum rate of interest rate and might not credit excess passion each year. Furthermore, the optimum withdrawal/surrender costs for an EIA are stated in the following table: Year 1Year 2Year 3Year 4Year 5Year 6Year 7Year 8Year 9Year 10Year 11 and Later10%10%10%9%8%7%6%5%4%3%0% A non-guaranteed index annuity, also typically referred to as an organized annuity, signed up index linked annuity (RILA), barrier annuity or floor annuity, is a buildup annuity in which the account worth increases or reduces as determined by a formula based on an exterior index, such as the S&P 500

The allowance of the amounts paid right into the agreement is normally chosen by the owner and might be transformed by the owner, subject to any legal transfer restrictions. The following are necessary attributes of and considerations in acquiring variable annuities: The agreement owner births the investment threat connected with properties kept in a different account (or sub account).

Withdrawals from a variable annuity may go through a withdrawal/surrender charge. You must be aware of the size of the charge and the length of the surrender charge duration. Starting with annuities marketed in 2024, the maximum withdrawal/surrender charges for variable annuities are established forth in the adhering to table: Year 1Year 2Year 3Year 4Year 5Year 6Year 7Year 8 and Later8%8%7%6%5%4%3%0%Request a copy of the program.

Tax Deferred Annuity Vs Ira

A lot of variable annuities include a death benefit equal to the greater of the account worth, the costs paid or the highest anniversary account worth - fixed income annuity good or bad. Several variable annuity agreements offer ensured living benefits that offer an assured minimum account, earnings or withdrawal advantage. For variable annuities with such ensured benefits, consumers should understand the costs for such benefit assurances in addition to any type of limitation or restriction on financial investments alternatives and transfer civil liberties

For fixed postponed annuities, the reward rate is included in the rate of interest declared for the very first contract year. Know exactly how long the reward rate will certainly be credited, the rate of interest to be credited after such perk rate period and any surcharges attributable to such reward, such as any type of higher abandonment or mortality and cost costs, a longer abandonment charge period, or if it is a variable annuity, it may have an incentive regain cost upon death of the annuitant.

In New York, representatives are called for to provide you with contrast types to aid you determine whether the replacement is in your best interest. Be mindful of the effects of replacement (new surrender cost and contestability duration) and make certain that the new product matches your existing requirements. Be skeptical of changing a delayed annuity that might be annuitized with an instant annuity without comparing the annuity repayments of both, and of replacing an existing agreement only to get a bonus offer on one more product.

Variable Annuity Income

Income taxes on interest and financial investment revenues in deferred annuities are delayed. In general, a partial withdrawal or surrender from an annuity before the owner gets to age 59 is subject to a 10% tax obligation penalty.

Usually, insurance claims under a variable annuity contract would be pleased out of such different account assets. If you purchase a tax obligation certified annuity, minimal distributions from the agreement are needed when you get to age 73.

Annuity Rate Chart

Only acquisition annuity items that match your needs and goals which are suitable for your economic and family situations. Make sure that the agent or broker is certified in excellent standing with the New york city State Department of Financial Providers. payout annuity definition. The Department of Financial Services has actually embraced regulations requiring agents and brokers to act in your benefits when making recommendations to you related to the sale of life insurance policy and annuity products

Be cautious of an agent who suggests that you authorize an application outside New York to buy a non-New York item. Annuity products authorized available in New York normally provide higher customer defenses than items sold somewhere else. The minimal account values are greater, costs are lower, and annuity payments and fatality benefits are extra positive.

Annuity Funded Life Insurance

Hi there, Stan, The Annuity Guy, America's annuity representative, certified in all 50 states. Are annuities truly guaranteed, Stan, The Annuity Man? Please tell us that Stan, The Annuity Guy.

All right, so allow's come down to the essentials. Annuities are issued by life insurance policy business. Life insurance policy business release annuities of all types. Bear in mind, there are several various kinds of annuities. Not all annuities misbehave out there, you haters. You already have one, with Social Protection, you could own 2 if you have a pension, but there are various annuity types.

Currently I have a couple of various methods I look at that when we're getting various annuity types. If we're getting a life time income stream, we're really weding that product, M-A-R-R-Y-I-N-G.

Generally, that's mosting likely to be A, A plus, A double plus, or better (fixed rate annuity fees). I take it on a case-by-case scenario, and I stand for basically every service provider around, so we're pricing quote all providers for the highest contractual guarantee. Currently if you're seeking principal defense and we're taking a look at a particular amount of time, like a Multi-Year Guaranteed Annuity, which is the annuity sector's version of the CD, we're not marrying them, we're dating them

Annuities Us

After that duration, we will either roll it to an additional MYGA, send you the money back, or send it back to the IRA where it came from. So, we're considering the Claims Paying Ability to ensure who's backing that up for that specific period. Follow me? Lifetime revenue, marrying the business.

As long as you're taking a breath, they're going to exist. Rate of interest, MYGAs, dating them. There may be a scenario with MYGAS where we're buying B dual plus carriers or A minus service providers for that duration because we have actually looked under the hood and deemed it ideal that they can support the case.

{kind=link}

Table of Contents

Latest Posts

Exploring the Basics of Retirement Options A Closer Look at Fixed Vs Variable Annuity Defining Fixed Annuity Or Variable Annuity Pros and Cons of Fixed Vs Variable Annuity Pros And Cons Why Choosing t

How Are Fixed Annuities Taxed

Highlighting Indexed Annuity Vs Fixed Annuity A Closer Look at Annuity Fixed Vs Variable Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Fixed Vs Variable Annuiti

More